Read the full story

Foundation brings unique insights on business, building product, driving growth, and accelerating your career — from CEOs, founders and insiders.

Is Growth Stage Venture Capital Dead?

Growth equity funding exploded five years ago and abruptly stopped this year. No boom times ahead.

Inbound investor inquiry—when venture capital funds cold email companies to pursue an investment—was common during 2020 and 2021. At the time, Albert, the company I run, was generating tens of millions of dollars in revenue. I received a lot of emails. Today, Albert is much bigger, profitable, and still growing quickly, but the inbound investor emails have long stopped.

A brief history

In its current format, growth stage venture capital is relatively new. Before VC funds exploded in size, companies had a few choices: (i) run profitably, (ii) sell, or (iii) enter the public markets by IPO, which were smaller and more frequent. This forced financial discipline on companies. Companies had to show meaningful revenue, sustained growth, and profit.

The financial crisis in 2008 triggered the Federal Reserve's zero interest-rate policy (ZIRP). Over the decade and a half that followed, investors stretched for returns, which spawned new asset classes.

One of these asset classes was growth stage equity. VC firms raised multi-billion dollar funds to invest in late stage, illiquid, pre-IPO startups. The basic pitch was that a 15% return is better than 0% earned on cash.

As ZIRP went on, late stage investing expanded beyond pre-IPO companies. By 2021, valuations soared to over 20x revenue, and in some cases much higher, with no differentiation between high and low gross margin businesses. Profitability was disregarded.

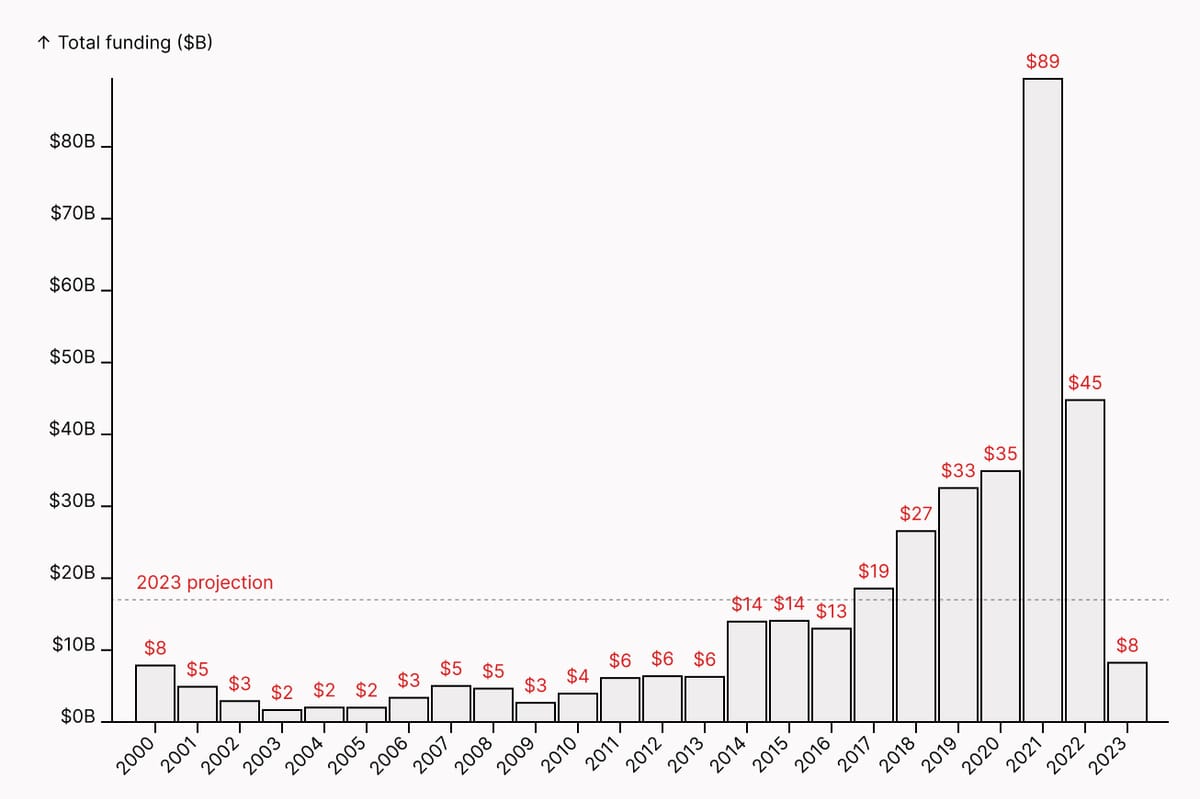

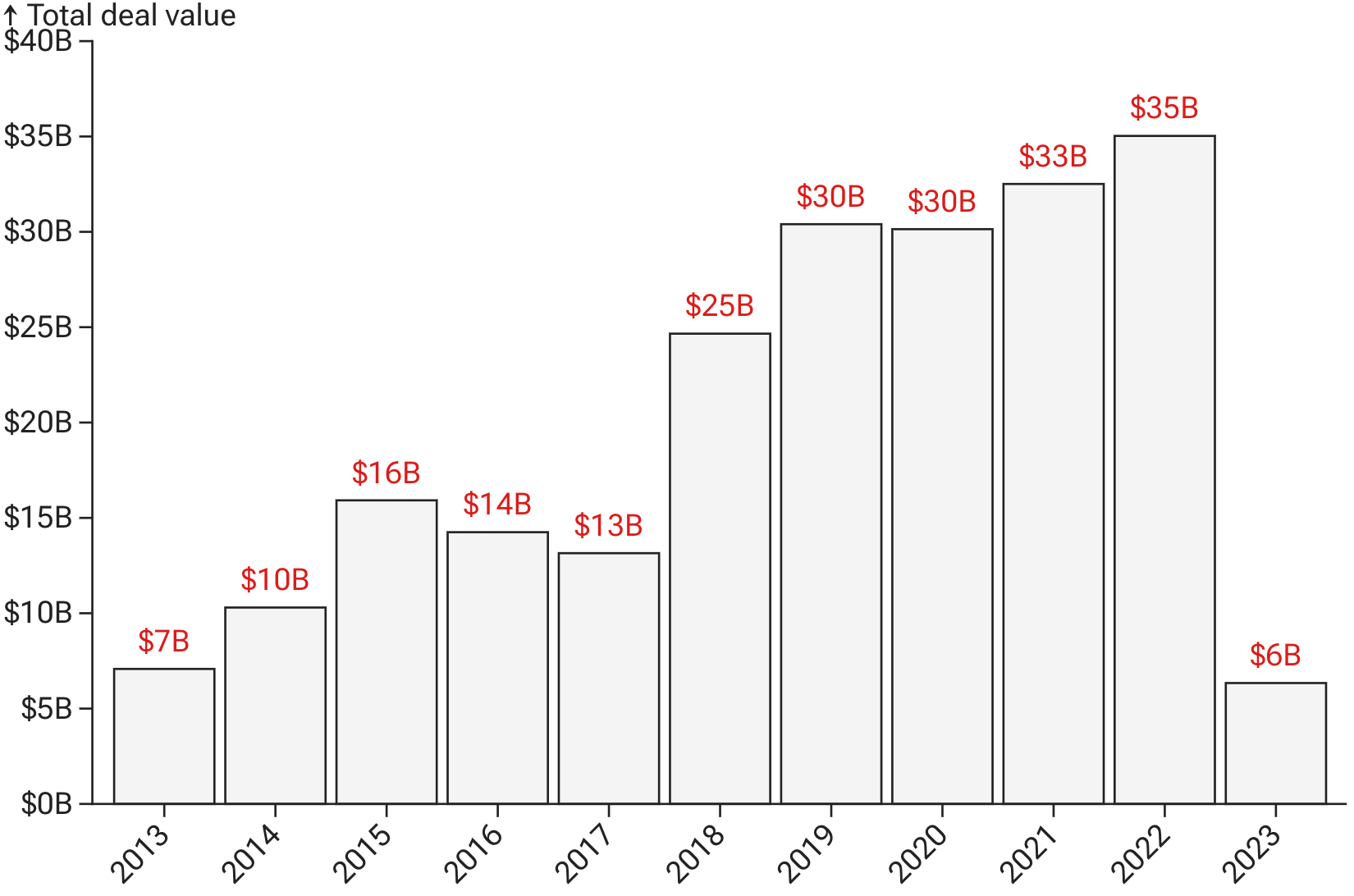

Series C and D capital raised in the U.S.

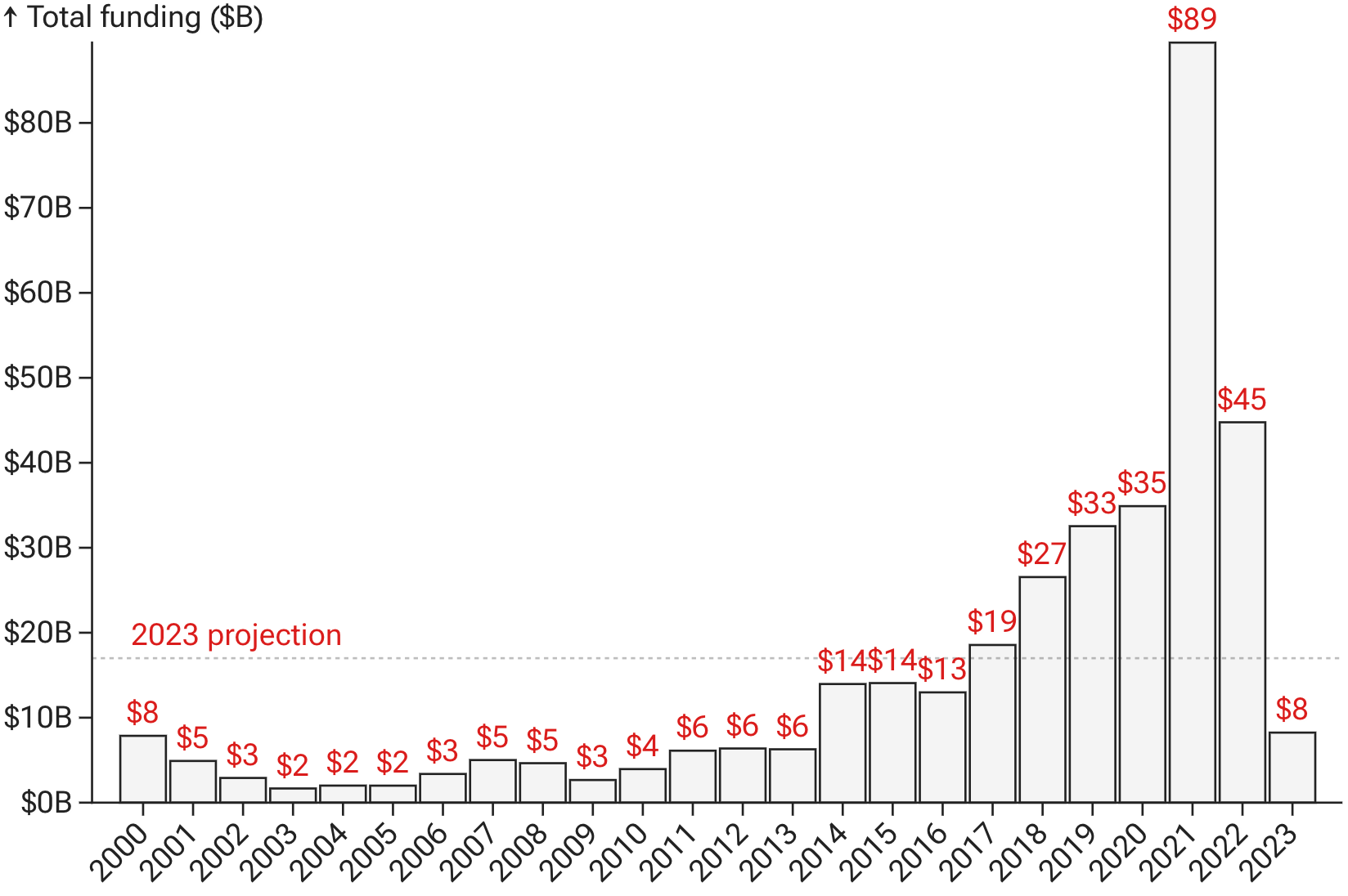

Number Series C and D deals in the U.S.

Interest rates rise

Growth stage venture capital investing has collapsed to pre-2017 levels.

Starting in 2022, the Fed raised the benchmark interest rate from 0% to over 5% in a year. Growth stage investments collapsed to pre-2017 levels. This happened for two reasons:

- The risk-free rate is now above 5%. Justifying the risk and illiquidity of investing in unprofitable sub-scale companies, years away from IPO, is now much more expensive.

- Exits stopped, which means investors can't get their money back.

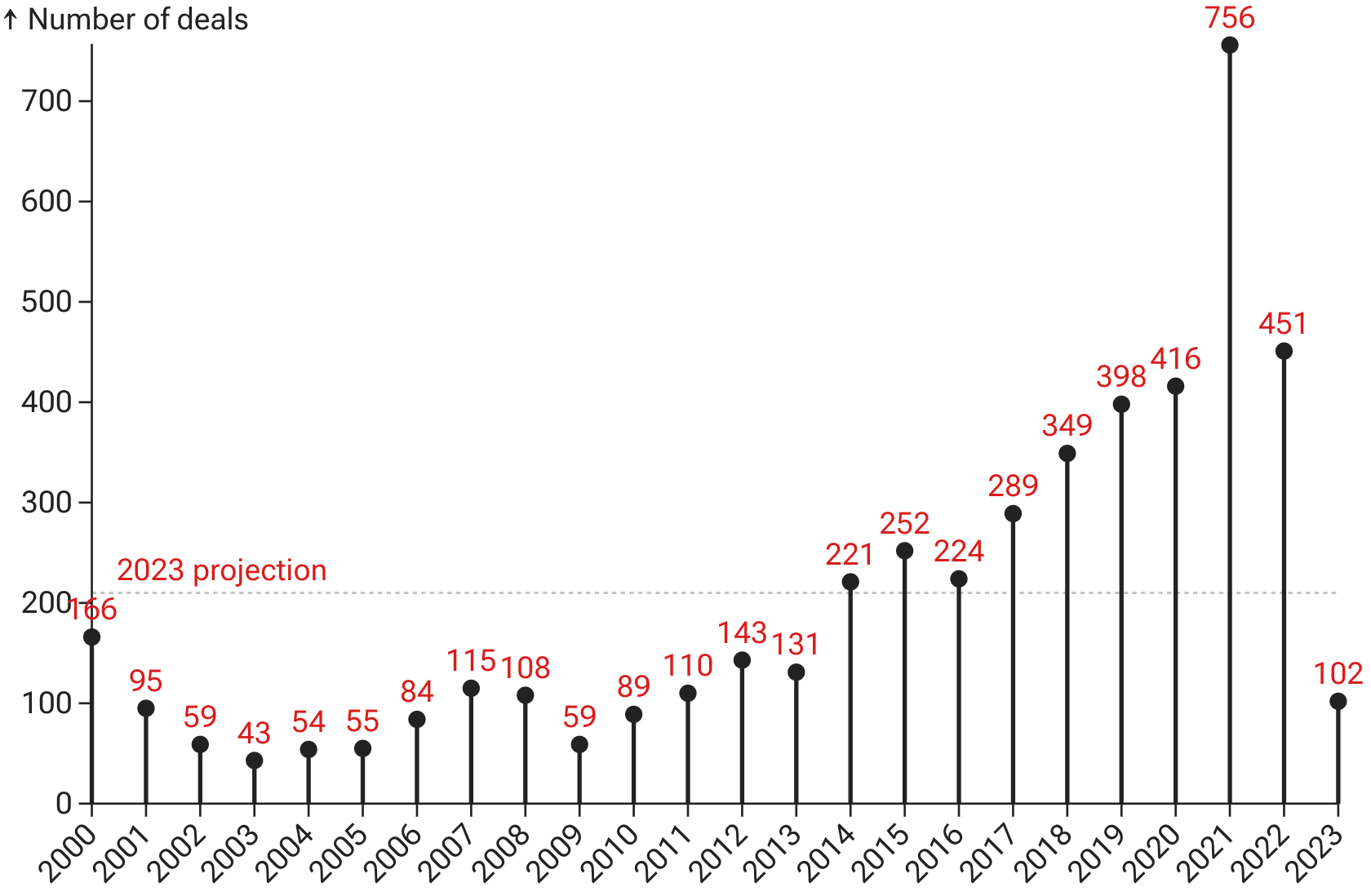

Exits for U.S. venture capital backed companies

IPOs and acquisitions nearly stopped in Q1 2022. Without a way to exit—either via sale or IPO—investors can't distribute money to the investors in their funds. Without a way to make money, funds stop investing in the asset class.

Venture debt

Borrowing money without a way to repay it is bad financial practice.

Venture debt is a term loan, usually provided to an unprofitable startup alongside an equity fundraise, that a startup can borrow at a later date.

The pitch to the startup is that it's a lifeline in a liquidity crunch; the pitch to the lender is that it's low risk despite the startup's operating metrics, because the startup has enough cash from an equity fundraise, and the startup will almost never need the money. But if the startup does borrow, it will be under duress, and it usually exacerbates a bad situation.

Not surprisingly, the venture debt market has also collapsed, on pace for 2014 levels. Borrowing money without a way to repay it is bad financial practice.

U.S. venture debt activity

Where to from here?

Once a company reaches a certain amount of revenue, it should be able to figure out how to stop losing money.

Investing in early stage startups accelerates invention. Investment dollars go towards fixed startup costs that a new business cannot afford, which significantly accelerates a company's timeline. But investing in an unprofitable business generating over $50 million of revenue only makes sense in a few situations:

- R&D: funding a project that a company cannot afford on its own. For example, hardware and biotech need capital to make new discoveries.

- Fund an acquisition: acquisitions can be financed by company stock, an equity investment or debt. All make sense in different situations and can also be used together.

- Market defining company: in rare situations, a company has the chance to change the behavior of tens of millions of people. Uber and AirBnb had this opportunity. This type of company can justify investing money in growing market share as fast as possible, profitability notwithstanding.

Aside from these situations, funding an operating loss at scale with investment dollars is a difficult way to make money. Once a company reaches a certain amount of revenue, it should be able to figure out how to stop losing money. If a company cannot break even, then the underlying economics of the business are not good, and additional outside capital masks the problem and prolongs it.

What happens next

Read the full story

Foundation brings unique insights on business, building product, driving growth, and accelerating your career — from CEOs, founders and insiders.